By Mark Anderson, CPA – US Tax Specialist for American Expats Abroad

After helping over 200 Americans navigate the Thailand Long-Term Resident (LTR) visa tax implications since the program launched in 2022, I’ve learned one thing: the biggest tax mistakes happen when people assume “tax-free in Thailand” means “tax-free everywhere.”

It doesn’t. Your US passport means Uncle Sam follows you to Chiang Mai, Phuket, and everywhere in between.

Let me walk you through exactly what the LTR visa does (and doesn’t do) for your US tax obligations—using real situations I’ve handled, not textbook theory.

What the LTR Visa Actually Is (And Who Gets It)

The Thailand Board of Investment (BOI) created the LTR visa in September 2022 to attract “high-potential” foreigners. Unlike tourist visas or even the expensive Elite Visa, the LTR is designed for people making Thailand their real home base.

The four LTR categories:

1. Wealthy Global Citizens

- Requirement: $1M+ in assets

- Must invest $500K in Thailand (property, bonds, or equity)

- Annual income $80K+ for past 2 years

2. Wealthy Pensioners (Age 50+)

- Requirement: $250K+ in assets OR $80K+ annual pension

- $40K annual income minimum

3. Work-from-Thailand Professionals

- Remote workers for established companies

- $80K annual income from foreign employer

- Employment in current company 1+ year

4. Highly Skilled Professionals

- Working for Thai company in targeted industries

- Different tax treatment (17% flat rate on Thai salary)

The visa gives you:

- 10-year residency (renewable)

- Multiple re-entry permit included

- Fast-track immigration lanes

- Work permit for same employer (Categories 3&4)

- And yes—tax benefits

But here’s what nobody tells you about those tax benefits…

The Thai Tax Perk (That Creates a US Tax Problem)

In January 2024, Thailand’s Revenue Department dropped a bomb on the expat community: all foreign income remitted to Thailand is now taxable.

This panicked thousands of expats who’d been bringing money into Thailand tax-free for years.

But LTR visa holders got a special exemption:

If you’re a Wealthy Global Citizen, Wealthy Pensioner, or Work-from-Thailand Professional, you pay ZERO Thai tax on foreign-source income—even when you bring it into Thailand.

(Highly Skilled Professionals get a different perk: 17% flat tax rate on their Thai salary instead of progressive rates up to 35%)

Sounds perfect, right?

Here’s the problem I explain to every LTR client:

When you pay zero Thai tax, you have zero foreign tax to credit against your US taxes. You can’t use the Foreign Tax Credit (Form 1116) because there’s no foreign tax paid.

Real example from my practice:

David, a Work-from-Thailand visa holder, earns $150,000 as a remote software engineer. Thailand: $0 tax due to LTR exemption. United States: $150,000 fully taxable unless we structure it correctly.

Without proper planning, David owes the full US tax bill with no offset.

This is where most “cheap” expat CPAs mess up—and where specialized guidance saves you thousands.

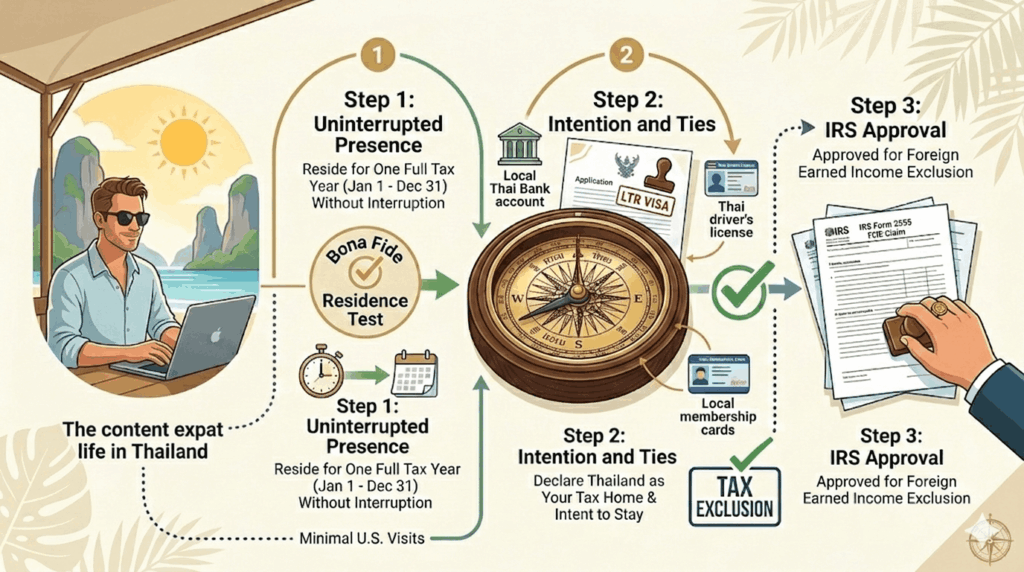

The Solution: Establishing Bona Fide Residence

The Foreign Earned Income Exclusion (FEIE) lets you exclude $120,000+ of foreign earned income from US taxes (adjusted annually—$126,500 for 2024).

To qualify, you must pass one of two tests:

Physical Presence Test:

- Be outside the US 330 full days in any 12-month period

- Rigid—one long trip home and you fail

Bona Fide Residence Test:

- Prove you’re a bona fide resident of a foreign country for a full tax year

- Much more flexible once established

This is where the LTR visa becomes a tax planning weapon.

Why LTR Strengthens Your Bona Fide Residence Claim

I’ve represented clients in IRS examinations where the agent questioned their Bona Fide Residence status. The LTR visa is powerful evidence because:

- 10-year commitment shows intent to remain (not temporary stay)

- BOI application process required proving substantial ties to Thailand

- Renewable status demonstrates long-term residency plan

- Investment requirements (for some categories) prove economic integration

Compare this to someone on annual visa extensions who might leave anytime—the IRS sees the difference.

Real case:

Jennifer, a Wealthy Pensioner LTR holder in Hua Hin, traveled to the US for 4 months to care for her sick mother. Under Physical Presence Test, she’d fail (more than 35 days in US).

But with established Bona Fide Residence via her LTR visa (plus Thai bank accounts, condo ownership, and local social ties), she maintained her FEIE qualification. She excluded $126,500 of her pension income, saving approximately $28,000 in US taxes.

The IRS accepted her position without challenge.

What the LTR Visa Does NOT Change

Let me be crystal clear about what the LTR visa doesn’t fix:

FBAR Still Required

If your Thai bank accounts (and other foreign accounts) total over $10,000 at any point during the year, you must file FinCEN Form 114 (FBAR).

The LTR visa doesn’t change this. Neither does living in Thailand for 20 years.

Penalty for non-filing: $10,000+ per year (non-willful) or 50% of account balance (willful).

I file 100+ FBARs annually for Thailand-based clients. It’s not optional.

FATCA (Form 8938) Still Required

If your specified foreign financial assets exceed thresholds ($200K-$600K depending on filing status), you must file Form 8938 with your tax return.

The LTR visa exempts these assets from Thai tax. It does not exempt them from US reporting.

Self-Employment Tax Still Applies

The FEIE excludes income from income tax. It does NOT exclude it from self-employment tax (15.3% on income up to ~$168,000).

Example from last month:

Carlos, a Work-from-Thailand LTR holder, works as an independent consultant earning $140,000. He properly claimed FEIE, excluding $126,500 from income tax.

But he still owed $21,462 in self-employment tax (15.3% on $140,000).

Many expats miss this. We explored S-Corp election to reduce his SE tax by approximately $8,000 annually—but that’s a whole separate discussion.

Passive Income Not Covered by FEIE

Investment income (interest, dividends, capital gains) doesn’t qualify for FEIE at all. With LTR exempting this from Thai tax, you pay full US tax rates with no offset.

We manage this through:

- Tax-loss harvesting

- Timing capital gains realizations

- Using US retirement accounts where possible

- Holding tax-efficient index funds

State Tax Considerations: The LTR Advantage

While living in Thailand, you still might face state tax claims from your former home state—especially “sticky” states like California, New York, Virginia, Massachusetts.

The LTR visa is powerful evidence of foreign domicile abandonment.

In domicile audits, states look for:

- Intent to remain abroad permanently

- Substantial ties to foreign country

- Lack of ties maintaining US state residency

A 10-year LTR visa checked multiple boxes:

- Long-term foreign residency plan

- Substantial Thai government approval process

- Economic ties (investment requirements for some categories)

Combined with:

- Selling US real estate

- Transferring financial accounts to Thailand

- Obtaining Thai driver’s license

- Registering with US Embassy in Bangkok

…you build a strong domicile termination case.

I’ve helped many clients successfully terminate California domicile using LTR visa as key evidence.

Strategic Tax Planning With LTR Status

Here’s how we optimize for clients with LTR visas:

1. Income Segmentation

Earned income (up to FEIE limit):

- Structured to maximize FEIE exclusion

- Thailand: $0 tax (LTR exemption)

- US: $0 tax (FEIE exclusion)

- Result: Zero global tax on first $126,500

Earned income above FEIE:

- Still Thai tax-free (LTR exemption)

- Fully US taxable

- Possibly subject to self-employment tax

- Consider S-Corp election if self-employed

Passive income:

- Thai tax-free (LTR exemption)

- Fully US taxable

- Manage through timing and structure

2. Retirement Income Planning

For Wealthy Pensioners with LTR status:

Social Security:

- Generally taxable only in residence country per US-Thai treaty (Article 19)

- With LTR exemption, often zero Thai tax

- May be partially taxable in US depending on other income

- Effective tax rate can be very low

Pension/401(k) Distributions:

- Thai tax-free (LTR exemption)

- Fully US taxable (no FEIE for pensions)

- No foreign tax credit (paid zero Thai tax)

- Strategic Roth conversions during low-income years

Example:

Robert, retired in Koh Samui with LTR, draws $60K from 401(k) and receives $30K Social Security.

- Thai tax: $0 (LTR exemption)

- US tax on 401(k): ~$6,500 (after standard deduction)

- US tax on Social Security: ~$1,500 (85% taxable)

- Total tax: ~$8,000 on $90K income = 8.9% effective rate

Compare to living in California: would pay ~$15,000.

3. Business Structure Optimization

For Work-from-Thailand entrepreneurs:

If self-employed with net income over $60K, S-Corp election typically saves $6,000-$12,000 annually in self-employment tax.

Process:

- Form US LLC or elect S-Corp status (Form 2553)

- Pay yourself reasonable W-2 salary

- Take remaining profits as distributions (no SE tax)

- Maintain proper payroll compliance

Trade-off:

- Additional complexity

- Payroll processing requirements

- Corporate tax return (Form 1120-S)

For most clients earning $80K+, the SE tax savings justify the cost.

Real Client Scenarios (Detailed)

Case 1: Remote Worker in Chiang Mai

Sarah, 34, Software Developer

- Income: $115,000 from US employer

- Visa: Work-from-Thailand LTR

- Living: Chiang Mai full-time (365 days/year)

Tax Analysis:

Thai Taxes:

- Foreign-source income: $115,000

- LTR exemption: 100%

- Thai tax due: $0

US Taxes:

- Gross income: $115,000

- FEIE (Form 2555): -$115,000

- Taxable income: $0

- Self-employment tax: $0 (W-2 employee)

Result: Zero global income tax

But watch out for:

- FICA/Medicare still withheld by employer (7.65%)

- Must file Form 2555 to claim FEIE

- FBAR required if Thai accounts >$10K

- Annual FEIE recertification

Case 2: Retiree in Phuket

Michael, 67, Retired Executive

- Income: $80K pension + $35K Social Security + $25K investment income

- Visa: Wealthy Pensioner LTR

- Living: Phuket 10+ months/year

Tax Analysis:

Thai Taxes:

- LTR exemption on all foreign income

- Thai tax due: $0

US Taxes:

- Pension: $80K (fully taxable—no FEIE for pensions)

- Social Security: $35K (85% taxable per provisional income calc)

- Investment income: $25K (dividends/interest—fully taxable)

- Total taxable: ~$135K

- Federal tax: ~$22,000

- No foreign tax credit (paid $0 Thai tax)

Result: $22K US tax on $140K income = 15.7% effective rate

Better than US:

- California would add ~$8K state tax

- Total US resident: ~$30K tax (21.4% rate)

- LTR saves ~$8K annually

Planning opportunities:

- Qualified charitable distributions (QCD) from IRA

- Tax-loss harvesting on investments

- Strategic Roth conversions in low-income years

Case 3: Digital Entrepreneur in Bangkok

David, 41, Online Marketing Consultant

- Income: $180,000 (self-employed)

- Visa: Work-from-Thailand LTR (structured consulting through foreign company initially, then independent)

- Living: Bangkok full-time

Tax Analysis:

Without optimization:

- Thai tax: $0 (LTR exemption)

- FEIE: -$126,500

- Taxable income: $53,500

- Income tax: ~$6,000

- SE tax on $180K: $27,672

- Total: $33,672 (18.7% effective)

With S-Corp optimization:

- Reasonable salary: $80,000

- Distributions: $100,000

- FEIE: -$80,000 (salary fully excluded)

- Taxable income: $100,000 (distributions—not earned income)

- Income tax: ~$15,500

- SE tax on $80K: $12,240

- Total: $27,740 (15.4% effective)

S-Corp saves ~$6,000 annually

Additional considerations:

- S-Corp setup cost: ~$2,000

- Annual compliance: ~$1,500

- Break-even income: ~$60K

- At $180K income, clearly worthwhile

Common LTR Tax Misconceptions I Correct Weekly

“I’m tax-free globally with LTR”

Truth: Tax-free in Thailand only. US taxes still apply with proper planning needed.

“I don’t need to file US taxes anymore”

Truth: US citizens file regardless of where they live. Period.

“LTR exempts me from FBAR”

Truth: FBAR is a Treasury filing, not IRS. LTR changes nothing about FBAR requirements.

“All my income is tax-free under FEIE”

Truth: FEIE only covers earned income up to limit ($126,500). Passive income fully taxable.

“I can use Foreign Tax Credit with LTR”

Truth: FTC requires paying foreign tax. LTR exempts Thai tax, so no FTC available.

“LTR makes my business tax-free”

Truth: Self-employment tax still applies. Business structure planning essential.

When LTR Visa Might NOT Be Worth It

Let me be honest: the LTR isn’t perfect for everyone.

Consider alternatives if:

You earn under $80K:

- Wealthy Pensioner might work

- But investment requirements may not justify benefits

- Regular retirement visa + proper tax planning might suffice

You travel frequently to US:

- LTR helps with Bona Fide Residence

- But if you’re in US 4+ months annually, complications arise

- Physical Presence Test might be easier

You have mostly passive income:

- LTR exempts Thai tax on passive income

- But US fully taxes it anyway with no offset

- Benefit is limited

You’re not committed to 10 years:

- Application process is intensive

- If you might leave Thailand in 2-3 years, regular visa may be simpler

Cost-benefit doesn’t work:

- LTR application: ~$3,000-$5,000 in fees/legal

- Thai tax savings vary by income type

- For some people, savings don’t justify complexity

The Application Reality (What Nobody Tells You)

The BOI website makes LTR sound simple. It’s not.

From my clients’ experiences:

Timeline:

- Application to approval: 2-6 months average

- Some approved in 4 weeks, others took 8 months

- No real pattern I’ve identified

Documentation required:

- Financial statements (bank, brokerage)

- Employment verification (notarized, apostilled)

- Background checks (FBI, local police)

- Health insurance (minimum coverage requirements)

- Everything translated to Thai if needed

Costs:

- Application fee: 50,000 baht (~$1,400)

- Legal assistance: $1,500-$3,000 (I recommend using specialist)

- Document preparation: $500-$1,000

- Health insurance: Varies

- Total: $3,000-$5,000+

Rejection reasons I’ve seen:

- Insufficient documentation of income/assets

- Employment verification issues (particularly for remote workers)

- Background check problems

- Insurance coverage gaps

One client spent $5,000 and 6 months, only to be rejected for incomplete employment verification. Reapplied successfully 8 months later.

My advice: Work with an experienced Thai visa agency for the BOI portion, and a US CPA (like me) for the tax planning portion. Trying to DIY often leads to mistakes.

How We Help

My process with LTR clients:

Phase 1: Pre-Application Tax Planning (Before you apply)

- Analyze whether LTR tax benefits justify your situation

- Calculate projected tax savings

- Compare to alternative visa/tax strategies

- Cost-benefit analysis

Phase 2: Documentation Support (During application)

- Prepare financial documentation for BOI

- Structure income statements for optimal presentation

- Coordinate with visa agent on tax-related questions

Phase 3: Implementation (After approval)

- File Form 2555 (FEIE) properly

- Establish Bona Fide Residence documentation

- Set up FBAR/FATCA compliance

- State tax domicile termination (if needed)

- Business structure optimization (S-Corp, etc.)

Phase 4: Ongoing Optimization (Annual)

- Yearly tax return preparation

- FBAR filing

- Strategic tax planning

- Monitor for tax law changes affecting LTR holders

- Adjust strategies as income changes

We’ve helped 200+ Americans with LTR tax planning since 2022.

Final Thoughts: Is the LTR Worth It?

For the right person, the Thailand LTR visa is a powerful tax optimization tool.

Best candidates:

- High earners ($100K+) with mostly earned income

- Remote workers employed by foreign companies

- Retirees with substantial pensions

- True long-term Thailand residents (5-10+ year commitment)

- People who were paying significant taxes in high-tax US states

The combination of:

- Thai tax exemption on foreign income (via LTR)

- US FEIE up to $126,500 (via Bona Fide Residence)

- State tax termination (via domicile change)

Can result in 10-20% effective global tax rates on six-figure incomes.

But it requires:

- Proper planning BEFORE application

- Correct annual compliance (FEIE, FBAR, FATCA)

- Strategic income/business structuring

- Professional guidance (Thai visa agent + US expat CPA)

Don’t go it alone. The tax mistakes I fix for LTR holders who tried DIY or worked with generalist CPAs cost them $10,000-$50,000 in unnecessary taxes and penalties.

Next Steps

Considering the LTR visa? Here’s what to do:

1. Get a tax projection Schedule a consultation with a US expat CPA (like me) to calculate your actual tax savings with LTR status vs. alternatives.

2. Don’t apply blindly Many people apply for LTR without understanding tax implications. Plan FIRST, apply SECOND.

3. Use specialists Thai visa agent for BOI application, US expat CPA for tax planning. Both critical.

4. Document everything Keep meticulous records of your Thai residency, ties, and intent. The IRS may question Bona Fide Residence years later.

5. Plan long-term LTR is a 10-year commitment. Think through tax implications if you leave Thailand, move back to US, or change income structure.

Ready to explore whether the LTR visa makes sense for your tax situation?

Contact Mark Anderson, CPA

Tel./WhatsApp: +16469611866

Email: mark@markandersoncpa.com

Line ID: marquenyc

I exclusively serve US expats Abroad. Let’s make sure your LTR visa works FOR you, not against you, from a tax perspective.

About Mark Anderson, CPA

Licensed US CPA with several years of experience serving American expats throughout Thailand. Based in Bangkok with clients in Chiang Mai, Phuket, Pattaya, Koh Samui, and beyond. Specializing in LTR visa tax planning, FEIE optimization, FBAR compliance, and expat business structuring.

Not a Thai tax expert—I focus exclusively on US tax obligations for Americans abroad.